NBFC Registration: An Alternate Lending System

A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 which engages in the business of loans and advances, acquisition of shares, stocks, bonds, debentures, and securities issued by the Government or a local authority or other related marketable securities, leasing, hiring-purchasing, insurance or chit business.

An NBFC does not include any institution whose principal business involves any sort of agriculture activities or industrial activities or purchase or sale of any goods (other than securities) or providing any services and sale/purchase/construction of any immovable property. In order to operate as an NBFC, a company requires NBFC Registration from the Reserve Bank of India (RBI).

Financial activity as “principal business” in the NBFCs

Any registered company which has financial activity as its principal business must fulfill two conditions:

- The company’s financial assets must constitute more than 50 percent of its total assets and

- The company’s income from financial assets must constitute more than 50 percent of the gross income.

This test is popularly known as the 50-50 test and is applied to determine whether or not a company is in financial business. If a company fulfills both these criteria, then it will be registered as an NBFC by the Reserve Bank of India. The Reserve Bank defines the ‘principle business’ to ensure that only companies predominantly engaged in financial activity get registered with the tag of being an NBFC registration and are regulated and supervised by the bank itself.

If some companies engage in agricultural operations, industrial activity, purchase and sale of goods, providing services or purchase, sale or construction of immovable property as their principal business and are doing some financial business in a small way, they will not be regulated by the Apex Bank.

NBFCs v/s Banks

A Non-Banking Financial Company can lend credit and make investments, in the same manner as the banks, but there are a few differences that differentiate an NBFC registration from the bank in their establishment, composition and working. Some of the differences are given below:

- An NBFC cannot accept demand deposits.

- An NBFC registration is relatively easy to establish because of lesser licensing requirements.

- An NBFC does not form any part of the payment and settlement systems.

- An NBFC cannot issue cheques drawn on itself.

- An NBFC can allow foreign investment of 100%, which is not the case with private banks.

- An NBFC cannot provide transaction services like banks.

- An NBFC is not required to maintain a reserve ratio, which is mandatory in the case of a bank.

- The deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not available to depositors of NBFCs.

Is registration for all NBFCs necessary?

As per the RBI Act of 1934, any Non-Banking Financial Company (NBFC) cannot commence or resume its business activities of operating a non-banking financial institution without

- Obtaining a certificate of registration of an NBFC registration for their company from the Apex Bank, and

- Having a Net Owned Fund of ₹ 10 crores.

But there are exceptions to this as well. In some cases, the Reserve Bank of India has the power to obviate these dual regulations, where certain categories of NBFCs are regulated by other regulators. Therefore, they are exempted from the requirements of registration with RBI. Some examples of such financial institutions are

- Venture Capital Fund

- Merchant Banking companies

- Stockbroking companies registered with SEBI

- Insurance Company with a valid Certificate of Registration issued by IRDA

- Nidhi companies notified under the Companies Act, 1956

- Chit companies defined in the Chit Funds Act, 1982

- Housing Finance Companies regulated by National Housing Bank

- Stock Exchange

- Mutual Benefit company

Actions against an operational non-registered NBFC

It is illegal for any financial entity which is an unincorporated body to make a false claim of being regulated by the Reserve Bank of India, misleading the public to collect deposits, and is liable for penalty action under the Indian Penal Code. Information in this regard may be forwarded to the nearest office of the Reserve Bank and the Police. If companies that are required to be registered with the Reserve Bank as NBFCs are found to be conducting a non-banking financial activity, such as lending, investment, or deposit acceptance as their principal business, without seeking registration, the Reserve Bank can impose a penalty or fine on them or can even prosecute them in a court of law. If members of the public come across any entity which does non-banking financial activity but does not figure in the list of authorized NBFC registrations on the RBI website, they should inform the nearest Regional Office of the Reserve Bank, for appropriate action to be taken for contravention of the provisions of the RBI Act, 1934.

Types of NBFC registrations

To serve different purposes, the RBI has categorized and defined different kinds of Non-Banking Financial Institutions. Let us look at some of them.

One can classify the NBFC registrations in the following ways:

Classification of NBFCs: Based on Deposits

Deposit-taking Non-Banking Financial Company ((NBFC-D)

Deposit Accepting NBFCs must get themselves registered with RBI as per the provisions in the RBI Act, 1934. They need a Certificate of Registration (CoR) from the RBI. And there are additional guidelines and specific regulations prescribed by RBI for them.

Non-Deposit taking Non-Banking Financial Company (NBFC-ND)

Non-Deposit Accepting NBFCs also need to get registered themselves. The only difference is additional guidelines do not apply to them

Further Classification of NBFC-ND

Systematically Important NBFC-ND

NBFCs whose asset size is ₹ 500 cr or more as per the last audited balance sheet are considered systemically important NBFCs. The rationale for such classification is that the activities of such NBFCs will have a bearing on the financial stability of the overall economy.

Asset Finance Company (AFC)

The financial institution with the primary business of financing physical assets.

Investment Company (IC)

It is a financial institution engaged in the acquisition of securities as of its principal business.

Loan Company (LC)

An Institution providing finance as its principal business. The business activity is to make loans or advances or otherwise for any ventures other than its own but does not include an Asset Finance Company.

Infrastructure Finance Company (IFC)

An NBFC-IFC is a company that:

-

- extends at least 75% of its total assets in infrastructure loans,

- has a minimum of Rs. 300 crores as Net Owned Funds,

- has a credit rating of not less than “A”, and,

- a CRAR of 15%.

Classification of NBFCs: Based on nature of Business Activity

Mortgage Guarantee Company

Mortgage Finance Company is the Non-Banking Financial Company whose-

- At least 90% of the business turnover of the Micro Finance Company is mortgage guarantee business or

- At least 90% of the gross income of the Micro Finance Company is from the mortgage guarantee business and,

- The net owned fund of the Micro Finance Company is Rs 100 crore.

NBFC-Non-Operative Financial Holding Company

Through Non-Operative Financial Holding Company, promoter/promoter groups will be authorized to set up a new bank. It is a type of NBFC registration that will hold the bank as well as all other financial companies regulated by RBI or other financial sector regulators, to the extent allowed under the applicable regulatory prescriptions.

Micro Finance Company

Micro Finance Companies in NBFC registrations are the companies that perform the functions similar to Banks. Loans are offered by the Micro Finance companies to various small businesses that do not have access to the formal banking channels and are not eligible for availing loans. MFI shall qualify the following criteria –

- 85%of qualifying assets are to be maintained all the time

- The loan disbursed by the Micro Finance Company to a borrower having annual income–

- In the rural sector not exceeding Rs 1,25,000or

- Urban and semi-urban not exceeding Rs 2,00,000.

- The amount of the loan shall not exceed Rs75,000 in the first cycle and Rs1, 25,000 in subsequent cycles. However, the tenure of the loan is not less than 24 months

- The total indebtedness of the borrower does not exceed Rs 1,25,000.

- Loans have to be provided without collateral.

- The repayment of the loan is at the choice of the borrower on a weekly, fortnightly, or monthly basis.

NBFC Factors

NBFC-Factor is a different type of NBFC registration engaged in the principal business of factoring. The financial assets in the NBFC Factor should aggregate at least 50% of its total assets, and also income acquired from the factoring business should be at least 50% of the gross income.

Systematically Important Core Investment Company

Systematically Important Core Investment Company is a type of NBFC registration that carries on the business of share (Equity and Preference) and securities acquisition but is subject to a condition that –

- It holds no less than 90% of its Total Assets as an investment in equity or preference shares, and debt or loans in group companies.

- Its investments in the equity shares (including instruments that would convert into equity shares within a period not more than 10 years from the date of issue, compulsorily) in group companies form at least 60% of its Total Assets.

- It does not invest in shares, debt, or loans in group companies except through block sales for dilution or disinvestment.

- No financial activities, as listed under Section 45I(c) and 45I(f) of the NBFC Act in RBI, are carried out by it. its asset size is Rs 100 crores or more, and,

- It accepts public funds.

- It should be noted systematically. Important Core Investment Companies do accept public funds.

Infrastructure Debt Fund NBFC

Infrastructure Debt Fund NBFC is a non-deposit-taking NBFC registration that deals in the facilitation of long-term debt into an infrastructure sector. Infrastructure Debt Fund NBFC raises the resources either through an issue of the rupee or dollar-denominated bonds of 5 years. IDF NBFCs can only be sponsored by Infrastructure Finance Company. The maturity period is of 5 years.

NBFC Account Aggregator

NBFC Account Aggregator is a new concept in NBFC registration. NBFC Account Aggregator provides data of several users and shifts their financial needs to various financial organizations. The activities of an Account Aggregator involve providing customers with financial information in a consolidated and retrievable manner to the customer. NBFC Account Aggregator provides reliable information.

NBFC Peer to Peer Lending Platforms

NBFC Peer-to-Peer lending platforms provide a platform to bring lenders and borrowers together by using a digital platform. It provides an opportunity for investors to diversify their portfolios. NBFC P2P has removed the cumbersome process of loans and has provided the ease of processing the loans. NBFC P2P Platform is the key player in the small business sector.

Housing Finance Company

Housing Finance Company is a form of NBFC registration with the principal business of financing of acquisition or construction of houses. HFCs are regulated by the Reserve Bank of India. A Housing Finance company cannot commence the business without obtaining a certificate of registration (CoR) from the Reserve Bank of India.

Eligibility Criteria For NBFC Registration with RBI

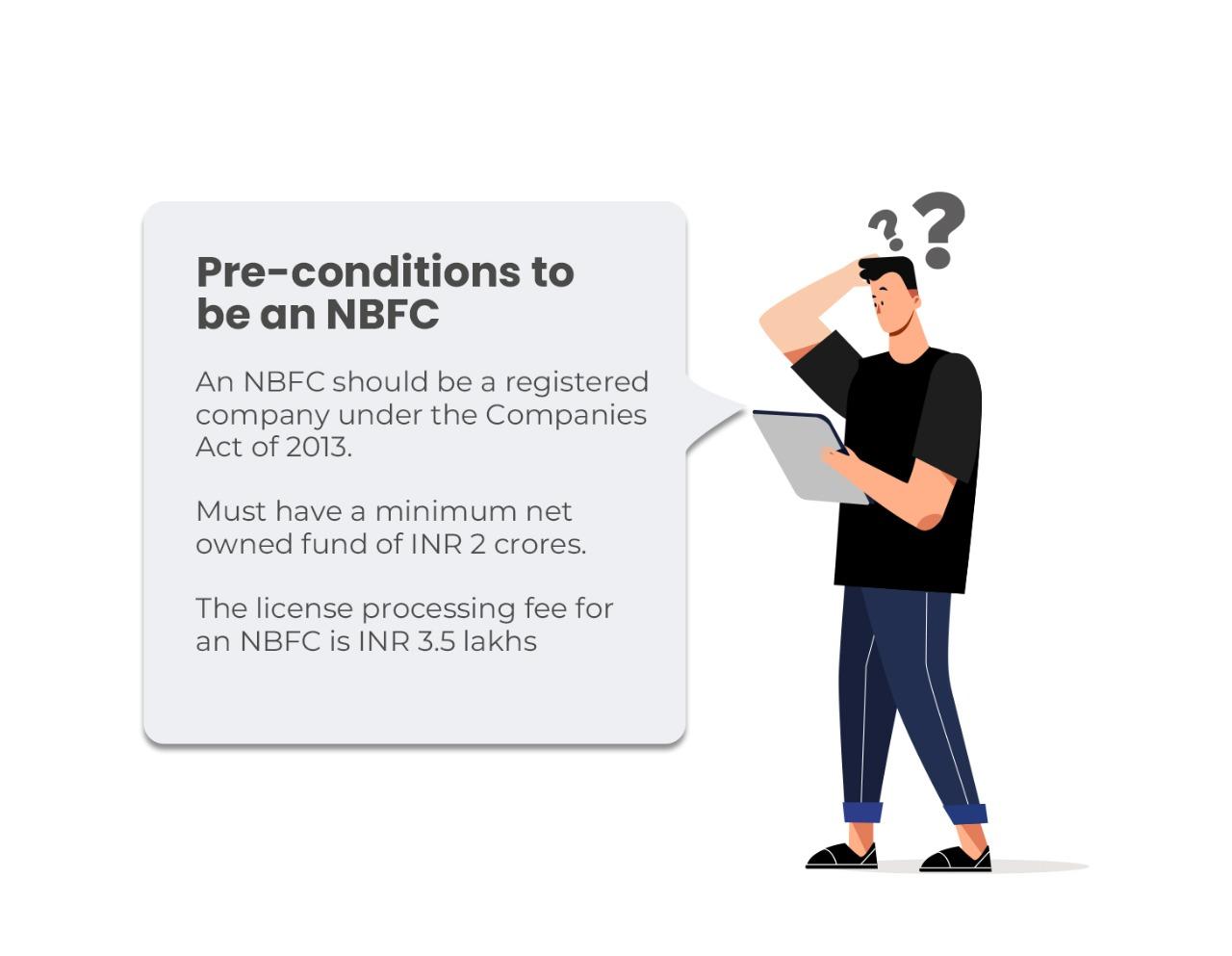

The applicant must be an incorporated company under the Companies Act, 1956 and desirous of commencing the business of a non-banking financial institution as defined in the RBI Act of 1934 should comply with the following:

- It should be a company registered under Section 3 of the Companies Act of 1956.

- It should have a minimum net owned fund of ₹ 10 crores.

NBFC Registration Process

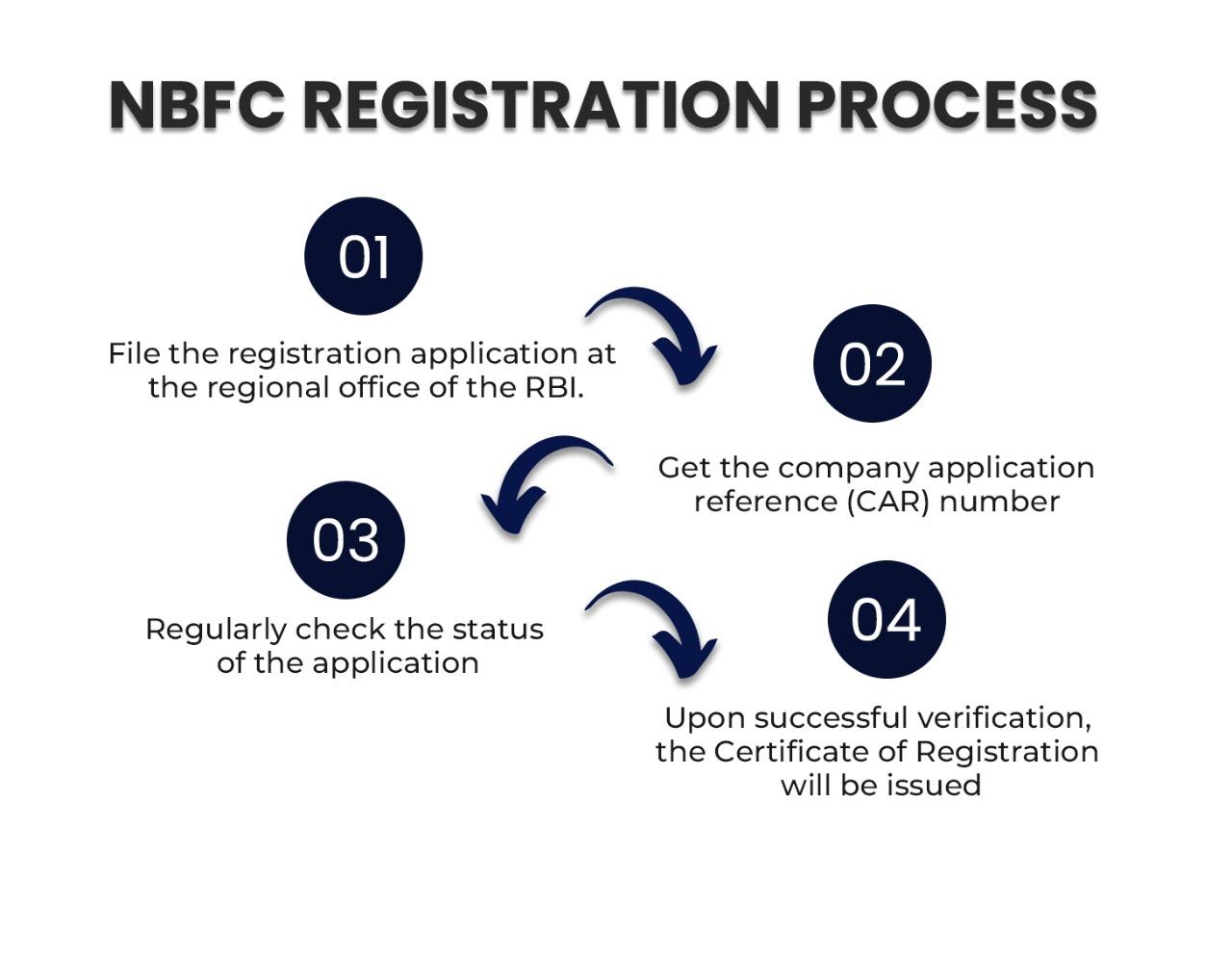

The applicant company can initiate the process of NBFC registration in the following manner:

- File the application online and submit a physical copy of the application along with the required documents to the Regional Office of the Reserve Bank of India.

- The application can be submitted online by accessing RBI’s website- https://cosmos.rbi.org.in. The company can click on “CLICK” for Company Registration on the login page of the COSMOS Application. A window showing the Excel application form available for download will be displayed.

- The company can then download their preferred application form (i.e. NBFC or SC/RC) from the above website, enter the data and upload the application form. The company may note to indicate the correct name of the Regional Office in the Excel application form.

- The company would then get a Company Application Reference Number for the CoR (Certificate of Registration) application filed online. Thereafter, the company has to submit the hard copy of the application form (indicating the online Company Application Reference Number, along with the supporting documents, to the concerned Regional Office).

- The company can regularly check the status of the application from the above-mentioned secure website, by keying in the acknowledgment number.

NBFC Registration Fee

The required processing fee for the NBFC registration of a license is approximately Rs. 3, 50,000 to register a company as NBFC with a Net Owned Fund of Rs. 10 crores. If you are opting for the professional expertise of an NBFC consultant, you have to additionally pay 10-12 lakhs rupees. Therefore, the total expenditure for you to procure an NBFC license could amount to Rs. 15-16 lakhs

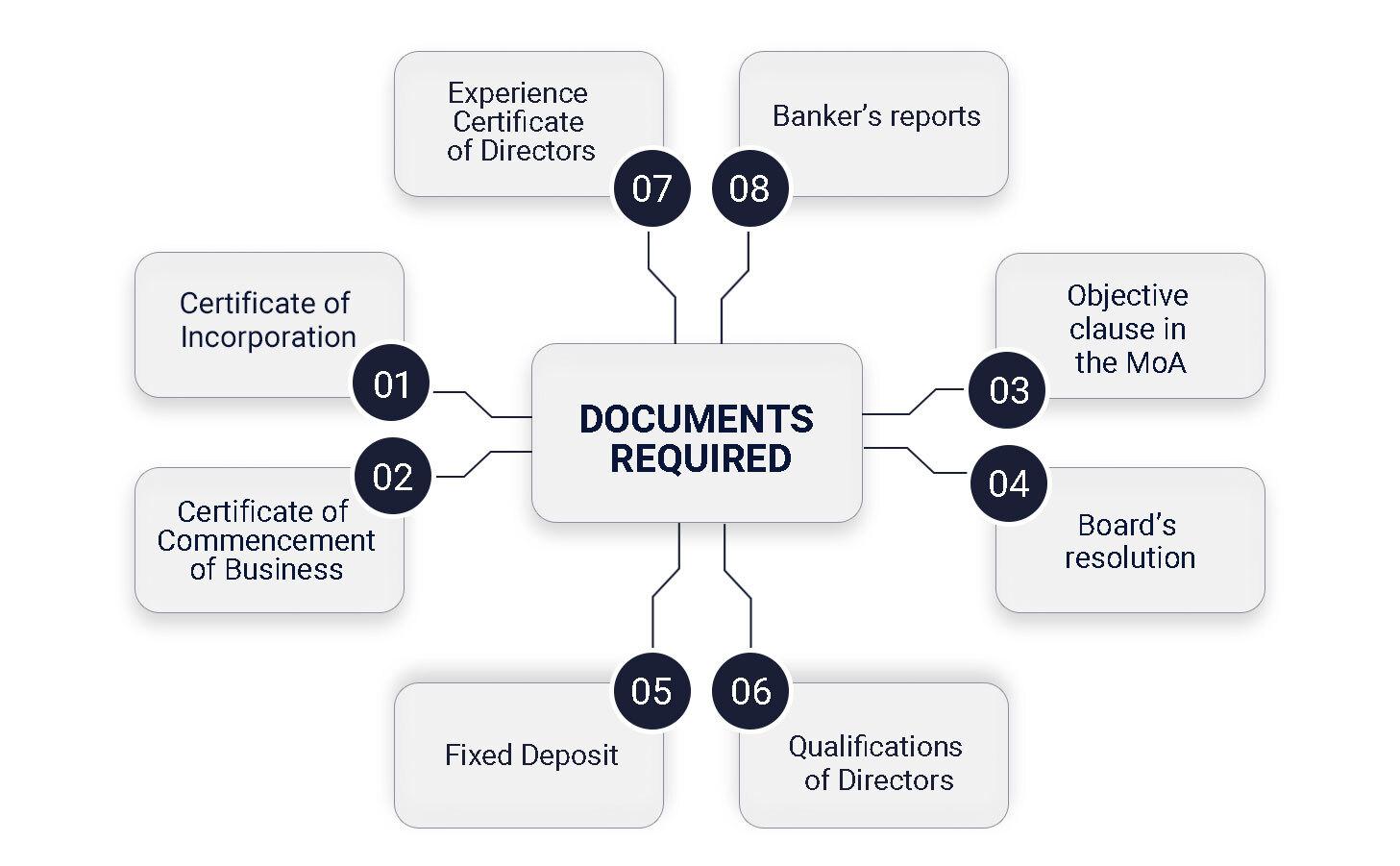

Documents checklist for NBFC registration

Below mentioned is the indicative checklist of the documents required to be submitted along with the application for the NBFC registration license.

- Certified copy of the CoI (Certificate of Incorporation) of the applicant company

- Certified copy of the CoCoB (Certificate of Commencement of Business) in case the applicant company is a PLC (Public Limited Company).

- Certified copies of the extract of the main objective clause in the Memorandum of Association relating to the financial business of the proposed NBFC.

- Resolution of the Board of Directors stating the following:

- The company is not carrying on any NBFC activity or has stopped any NBFC activity and will not carry on or start the same before getting license registration from the RBI.

- The company has not accepted any public deposit, in the past and does not hold any public deposit as of the date, and will not accept the same in the future without the prior approval of the Reserve Bank of India

- The UIBs in the group where the director holds a substantial interest or otherwise has not accepted any public deposit in the past and does not hold any public deposit as of the date and will not accept the same in future

- The company has formulated a “Fair Practices Code” as per the RBI Guidelines

- Copy of Fixed Deposit receipt & bankers certificate of no lien indicating balances in support of Net Owned Funds (NOF).

- For companies already in existence, the audited balance sheet and Profit & Loss account along with directors & auditors report or for the entire period the company is in existence, or for the last three years, whichever is less should be submitted.

- Copy of the certificate of highest educational and professional qualification in respect of all the directors.

- Copy of experience certificate, if any, in the Financial Services Sector (including Banking Sector) in respect of all the directors.

- Banker’s reports in respect of the applicant company, its group/subsidiary/associate/holding company/related parties, and directors of the applicant company having substantial interest in other companies. The Banker’s report should be about the dealings of these entities with these bankers as a depositing entity or a borrowing entity.

The applicant has to provide bankers' reports from all the bankers of each of these entities and provide the report for all the entities. The details of deposits and loan balances as on the date of application and the conduct of the account should be specified.

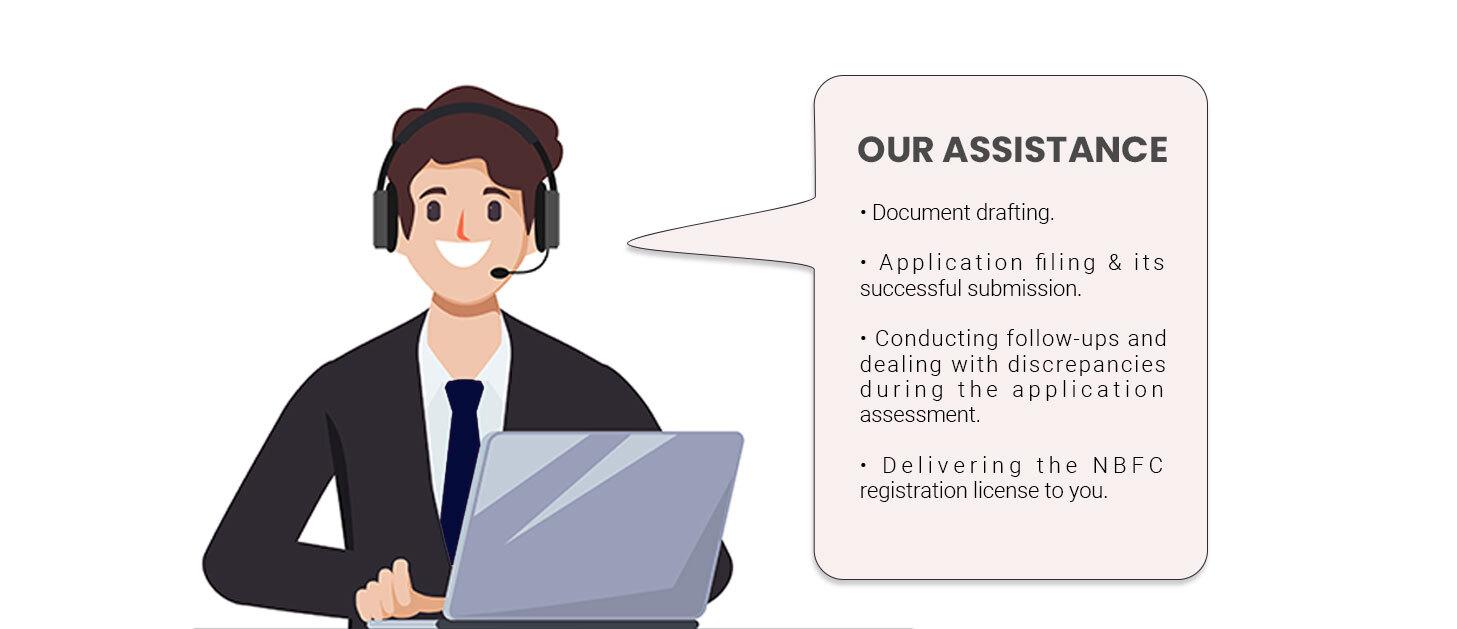

Our Assistance to get the NBFC Registration in India

Registrationwala can assist you with the NBFC license registration for your business by providing you with the following services:

- Document drafting.

- Application filing & its successful submission.

- Conducting follow-ups and dealing with discrepancies during the application assessment.

- Delivering the NBFC registration license to you.

So, connect with us if you want the NBFC Registration for your company in a time and cost-effective manner.

FAQs

Q.1) What is an NBFC license?

A. It is a legal permit issued by the RBI authorizing its license holder to commence or

resume its Non-Banking financial services to its clients/customers.

Q.2) Are NBFCs regulated by RBI?

A. Yes. The NBFCs are regulated under the RBI act of 1934.

Q.3) What are the NBFC registration requirements?

A. An NBFC must be a registered company under the Companies Act and

must have a net owned fund of INR 10 crores.

Q.4) How to check for the NBFC registration number?

A. The list of registered NBFCs is available on the website of the Reserve Bank of India

and can be viewed at www.rbi.org.in → Sitemap → NBFC List.

Q.5) How does one define a Non-Banking Financial Company (NBFC)?

A. A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 which engages in the business of

- Loans and advances

- Acquisition of shares, stocks, bonds, debentures, and securities issued by the Government or a local authority or other related marketable securities

- Leasing

- Hiring-purchasing

- Insurance business

- Chit businesses